Buyer's FAQ

What Should I Do First When Buying a Home?

Step One: talk to Us!

Don’t feel overwhelmed — talk to us! Our initial consultation is completely free, and we’ll walk you through the essentials: budgeting, market trends, neighbourhood insights, and programs like the First Home Savings Account (FHSA). No commitment required.

Step Two: get pre-approval for a mortgage.

Knowing whether you qualify for a mortgage – and for how much -takes away the guesswork and helps you focus on homes within your real budget.

Step Three: Connect with a real estate agent.

Finding the right real estate agent is essential, as they are your primary advocate and expert guide throughout the entire home-buying journey.

What is mortgage pre-approval, and why does it matter?

Mortgage pre-approval is a conditional commitment from a lender (like a bank or mortgage broker) to lend you a specific maximum amount of money for a home purchase, based on a full review of your finances.

Pre-approval is important because it:

- Shows your real budget:

You’ll know what price range you should be shopping in, instead of guessing. - Locks in Your Interest Rate (Protects You):

Most pre-approvals come with a Rate Hold for a set period (usually 90 to 120 days). - Strengthens Your Offer (Competitive Advantage):

A pre-approval letter shows sellers you’re serious and financially prepared. - Helps avoid surprises:

If there are any issues with your credit, income, or documents, you can find out early and fix them before you write an offer. - Speeds Up the Final Process (Faster Closing):

When you do find the right home, you’re already a few steps ahead with your financing.

Do I need to hire a real estate agent?

Hiring a real estate agent isn’t mandatory, but it can make the process much smoother. A licensed Edmonton agent can guide you through the market, negotiate for you, and help ensure all legal details are handled correctly. Without that support, you may miss key insights and important protections.

The best part? Buyers usually don’t pay the real estate commission. The seller covers the buyer’s agent fee, so you get expert guidance and negotiation support at no extra cost to you.

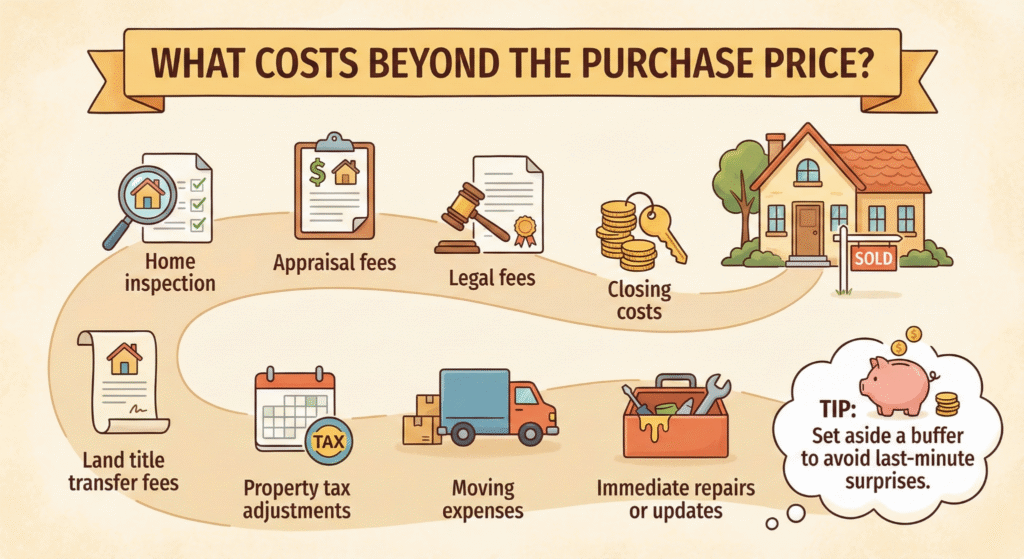

What costs should I expect when buying a home in Edmonton?

Besides the purchase price, it’s highly recommended to set aside money for the following three main categories of expenses:

1 Upfront & Down Payment Costs

- Down Payment: Your cash payment to secure the property (usually 5% minimum).

- Closing Costs: Fees paid on possession day (budget 1.5%–4% of the purchase price).

2 Required Professionals & Reports

- Legal Fees: Your lawyer’s fees for handling the transaction and disbursement costs.

- Inspections: Home inspection and appraisal fees.

- Registration: Land title registration fees.

3 Post-Move Essentials

- Home Insurance: A full year of coverage is required.

- Property Taxes: To reimburse the seller and start your own payments.

- Moving Costs: Paying for movers or truck rental.

- Utility Hookup/Deposits: Fees to start services like gas, electricity, and internet.

- Immediate Repairs/Maintenance: Funds for any small repairs, new locks, or necessary painting before you move in.

How much do I need for a down payment?

In Canada, the minimum down payment starts at 5%.

- 5% for homes up to $500,000

- 10% on the portion from $500,000–$999,999

- 20% for homes $1 million+

Putting down 20% or more lets you avoid mortgage default insurance (CMHC insurance), which lowers your monthly payments.

How do I choose the right neighbourhood for me?

When choosing a neighbourhood, think about your lifestyle and long-term needs. Consider things like:

- Commute and convenience.

How close is it to work, transit, shopping, or daily essentials? - Schools and family needs

Are there good schools, parks, or family-friendly amenities nearby? - Safety and community feel.

Do you feel comfortable in the area? Does the neighbourhood match your vibe? - Future plans.

Are you planning for kids, wanting walkability, or looking for a quieter area - Home styles and pricing.

Does the neighbourhood offer the type of homes and price range you’re aiming for?

Let us help you compare communities, understand market trends, and find the area that fits you best.

What is home buyer’s plan (HBP)?

The Home Buyer’s Plan allows first-time buyers to withdraw up to $60,000 from their RRSP tax-free upfront and repay it gradually over 15 years.

What is First Home Saving Account (FHSA)?

What it is:

A tax-free savings account specifically designed for buying your first home.

How it works:

- You can contribute up to $8,000 per year, to a lifetime maximum of $40,000.

- Your contributions are tax-deductible (like an RRSP).

- Withdrawals used to buy your first home are completely tax-free (like a TFSA).

- You can combine it with the Home Buyer’s Plan for even more down payment power.

Why it’s amazing:

It gives you two layers of tax benefits — saving on taxes when you contribute and paying zero tax when you withdraw.

What is the difference between a fixed-rate and a variable-rate mortgage?

A fixed-rate mortgage locks in your rate, so your payments never surprise you.

A variable-rate mortgage moves with the market – great when rates are low, but riskier when they rise.

What are closing costs, and how much should I budget for them?

Closing costs are the final fees you pay when the home officially becomes yours—things like your legal fees, disbursements, title insurance, land transfer taxes and lender charges. In Alberta, a safe estimate is 1.5% – 4% of the home’s price.

Real Estate 101: Simplified. Visualized. Demystified.

The Buyer’s FAQ doesn’t stop here. We have meticulously summarized and organized every common question you might encounter on your real estate journey. Whether you’re a first-time buyer, a relocator, or a seasoned investor.

Want your answers to look like this? Claim your FREE Real Estate 101 FAQ today!